📈 Production and Cost in Economics: A Complete Guide

In economics, production and cost analysis form the backbone of business decision-making. These concepts help firms determine how much to produce, at what cost, and how to maximize profits efficiently. Whether you’re a student, an entrepreneur, or simply curious, understanding these fundamentals is essential.

📌 What is Production in Economics?

Production refers to the process of transforming inputs (like labor, capital, and raw materials) into outputs (goods or services). The goal is to add value to the inputs and generate something that meets consumer demand.

🔹 Types of Production:

-

Primary Production – Extracting natural resources (e.g., farming, mining).

-

Secondary Production – Manufacturing and construction.

-

Tertiary Production – Services like education, transport, and healthcare.

🔹 Factors of Production:

-

Land – Natural resources.

-

Labor – Human effort (physical or mental).

-

Capital – Tools, machinery, infrastructure.

-

Entrepreneurship – Organizing resources to produce goods and services.

📊 The Production Function

A production function shows the relationship between input and output.

Example:

Q=f(L,K)

Where:

-

= Quantity of output

-

= Labor input

-

= Capital input

It helps firms understand how much output can be produced with different combinations of inputs.

🔄 Short Run vs Long Run in Production

1. Short Run:

-

At least one factor of production is fixed.

-

Typically, capital (machines, buildings) is fixed, while labor is variable.

2. Long Run:

-

All factors are variable.

-

Firms can adjust all inputs for optimal efficiency.

📉 Laws of Production

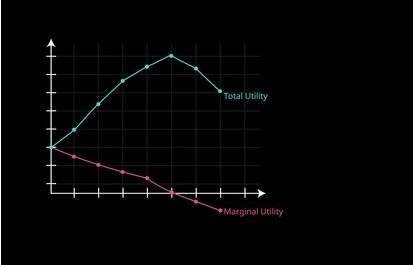

1. Law of Variable Proportions (Short Run):

As more units of a variable factor (like labor) are added to a fixed factor (like land), the marginal product initially increases, then decreases.

-

Increasing Returns – More output per input.

-

Diminishing Returns – Output grows slower than input.

-

Negative Returns – Output declines.

2. Returns to Scale (Long Run):

-

Increasing Returns to Scale – Doubling inputs more than doubles output.

-

Constant Returns to Scale – Output doubles when inputs double.

-

Decreasing Returns to Scale – Output increases less than inputs.

💰 What is Cost in Economics?

Cost refers to the expenditure incurred by a firm to produce goods or services. Understanding cost behavior is crucial for pricing, budgeting, and profit planning.

📚 Types of Costs:

🔹 Fixed Cost (FC):

-

Do not vary with output (e.g., rent, salaries).

-

Present even at zero production.

🔹 Variable Cost (VC):

-

Change with the level of output (e.g., raw materials, wages).

🔹 Total Cost (TC):

TC=FC+VC

🔹 Average Cost (AC):

🔹 Marginal Cost (MC):

-

Cost of producing one extra unit of output.

📈 Cost Curves Explained

-

Short-run cost curves: U-shaped due to the law of variable proportions.

-

Long-run cost curves: Also U-shaped, reflecting economies and diseconomies of scale.

🏭 Economies of Scale

As production increases, the cost per unit may decrease due to:

-

Bulk purchasing

-

Better technology

-

Managerial specialization

Diseconomies of Scale:

-

Occur when cost per unit increases due to:

-

Communication problems

-

Management inefficiencies

-

Over-expansion

-

🧠 Conclusion

Understanding production and cost helps firms optimize output and minimize costs, which is key to profitability and competitiveness. For students, these concepts are foundational to microeconomics and managerial economics.